House Prices and Bubbles

Property has always been a coveted asset in Australia and in the west for some really great reasons.

The family home, as well as a real estate portfolio, will always be the largest form of investment most Australians will ever indulge in.

For the last thirty years, Australian housing has solidified a reputation as a form of high gain asset, which is relatively “risk free”.

We hate the term “risk free” since its loaded with so many presuppositions of sometimes inane proportions.

Any form of investment (leaving money in the bank or under your bed is not an investment) has an element of risk.

Like life itself.

But with a great team advising you, the risk is obviously lowered to a great degree.

How else can you purchase a sizeable asset(that increases in value) with only a small deposit, with the banks providing the rest of the money ?

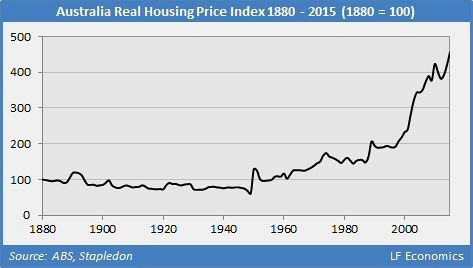

From 1996 to 2014, Australian housing prices, even when adjusted for quality/inflation etc, have risen by over 140%.

Other housing markets in Europe and Asia, “corrected” their prices/values after the global financial crisis, but Australia`s prices just kept on accelerating.

Now we realise that numerous Federal and state actions have intervened to make housing look highly attractive to investors.

Albeit helped as well by willing banks and financial institutions.

The banks, for some strange reason are sometimes called rapacious” for having the “temerity” lend people money for their investments.

And that`s bad is it ?

On a slight, but pertinent segue, there was a short piece on the ABC a few months ago where a couple was complaining about a nasty bank that had been lending them more money than they could actually pay back.

And when they failed to pay the interest on the money they greedily took, the bank became the “bad guy”.

Is Australia in any form of real estate “bubble” when you look at it overall.

And the simple answer is no.

What we believe many commentators are doing is misunderstanding that the sheer weight of population in Sydney and Melbourne skewers the average price badly.

But its trendy to call it a bubble for several reasons.

The governments immigration targets are pushing more and more people into the two major capital cities.

Limited amounts of houses and units , which are not being produced fast enough and bang, prices keep spiraling upwards in those two capital cities.

Which is one of the reasons why we, at Ample Property Solutions are not advising our clients to invest in Sydney or Melbourne at this stage.

Or the same doom merchants point to the US housing bubble and collapse with the either stated or heavily implied analogy being, it will happen here.

Lets have at look at that hip meme.

Fraudulent lending to residential borrowers was a key factor in the US housing bubble post-2006, when a large and insolvent subprime mortgage cohort was revealed by the collapse in land prices.

Finance was extended to millions of Americans without the proper assessments of their capacity to finance debt payments.

It was further fueled by a variety of exotic and bizarrely named mortgages which neither the banker or the lender understood.

Option ARMs,2/28 Hybrid ARMS and ALT-A loans etc.

Mind you, the banker who didn’t understand the toxic loan, did not care because he was making a bomb of money either way.

And Ronald Regan had loosened the regulations so that banks were less accountable.

Some of these loans had “honeymoon” periods of low interest rates for a few years before the borrower was hit by a huge hike.

And do not forget”NINJA” loans, where aspiring owner-occupiers and investors without an income, job or assets were provided with mortgages they were clearly unable to service.

Banks used creative accounting to manipulate loan application forms (LAFs) and inflate assets and incomes, fabricating a positive assessment of borrowers’ capacity to service much larger loans than was possible.

And so you had assets whose real worth was $X, yet their values on paper,were often three or four times that.

A very interesting film about a real life stock investor and interesting eccentric Michael Burry and his betting the US subprime would collapse is The Big Short.

Now we understand that when you look at the rate of growth of household debt in Australia and compare it to America, our household debt since 1990 has grown three times faster than American debt.

But how the hell any of those bizarre US situations and oversights is applicable to Australia is beyond us.

Land values in different parts of Australia, like everything, rise, stabilise, go down a little etc.

Then start the cycles again.

Nothing in life is static, yet doom merchants try and link one horrendous fraud(whose ramifications are still ongoing in the US) to countries like Australia.

Which is insane.

The time to take action is NOW.

Ample Property Solutions can help you with every step of the way.

Why not come to our next seminar in Sydney -Leichhardt – July 27th Wednesday- 2016

In the Evening ! Book HERE